Innovation is a loaded term that implies all sorts of sexy new business success. Hot new products, buzzy new technologies, founders on the cover of magazines – you get the idea. Everyone wants to be the hero entrepreneur. At least superficially.

The term innovation theater was coined by Steve Blank to describe splashy innovation programs that rarely deliver shippable/deployable product, found in organizations ranging from SMEs to large multinationals.

The scenario typically plays out like this:

Executives launch a flashy new innovation program surrounded by a lot of buzz. These executives eagerly want to believe that shortcuts are available to skip the normal investments of time + money. But the project gets messy fast and the executives soon realize they have little appetite for the challenges and risks inherent in taking a novel idea from concept to revenue. They lust after the superficial aspects of innovation programs — but as reality sets in, they slowly abandon the effort.

The root causes of innovation theater occur when senior level leaders – who should have extensive program management and scoping expertise under their belt – refuse to recognize three key realities in starting up the innovation program. They:

- Refuse to Recognize Realistic Customer Acquisition Costs

- Refuse to Recognize Realistic Project Development Costs

- Refuse to Recognize Realistic Time to Revenue

These three specific behaviors are neither accidental nor rookie mistakes. So let’s call these the 3 Sins, since these are such willfully ignorant behaviors.

Let’s dive into each of the three:

Sin 1: Refusal to Recognize Realistic Customer Acquisition Costs

Customer Acquisition Cost (CAC) is a metric now in widespread use for digital commerce and SaaS platforms, but one that is not usually considered in traditional B2B companies.

Ask yourself a tough question: If your Sales and Marketing teams exist to generate new customers, then simply add up all you spend on Sales and Marketing (salaries, overhead, cash outlays, channel partner fees, etc.) and divide that by the number of new customers you won (actual paying customers, not sales prospects).

Ouch!

In B2B environments, when asking a senior leader what their CAC number really is, it usually takes a couple beats before they return a look of disbelief of how big it is, and almost immediately start making excuses about why it somehow isn’t an appropriate metric. But how is it not?

And that lack of internalization of the true CAC cost will lead to the new innovation program being held to grossly unrealistic expectations. If your mainline business is actually investing $100k CAC to win each new customer (or whatever shockingly big number that turns out to be), how can you expect the new innovation team to win new customers for only $10k each? Or $1K?

Sin 2: Refusal to Recognize Realistic Project Development Costs

Big companies have lots of “resources”, right? So why can’t the innovation team make use of these “resources” to cut down their innovation program costs? This widely pervasive falsehood drives leaders into starving a venture team of real resource commitments. Let’s expand this a bit:

Availability of Resources

If you as a management team are running a tight ship, do your various functional teams have people just sitting around eagerly waiting to help out a new innovation team? Of course not! But leaders desperately want to believe that innovation programs can “leverage” these “available” resources. Worse, they then provide no incentives for the other functions to share in the risk of the innovation program – so those managers naturally don’t want to commit any of their precious resources to the program.

No Real Cost Controls

Unlike most consulting firms that require their employees to keep a timecard and closely keep track of all assignable project expenses, in many product development companies, no one really knows where the resources are actually being spent. Asking managers, engineers, marketers, etc. to start submitting a timecard or tracking expenses provokes intense resentment, as if you’re imposing some dystopian big brother program. This conveniently lets various managers hide the real efficacy of their development programs in general SG&A budgets, letting sloppy roadmap management and pet projects run rampant.

Yet when the company starts some splashy new product team or venture, typically the project will be separately budgeted and intensely tracked and reviewed.

False Cost Comparisons

This leads to the management team effectively comparing these discrete, highly visible innovation development programs against their nebulous, hidden, bloated traditional development programs. You’d be amazed at how often no one really wants to admit how much the legacy businesses actually cost, and how that blind attitude is enshrined in the financial tracking for the firm. Many times, especially with discrete corporate ventures, the effective cost of starting an entirely new business will be compared against the few CAPEX cost items that are discretely tracked in the existing businesses. So the venture looks ridiculously profligate.

Sin 3: Refusal to Recognize Realistic Time to Revenue

You know that old program management exhortation: Take whatever you think the schedule should be, double it, then double it again. Why do many executives hold innovation programs to such unrealistic expectations of time-to-revenue? Let’s break down three prime causes:

Structural Impatience

The hyper-driven executives who climb corporate ladders typical get 2-3 years in a role before being moved up or out. This leads to them kicking off new innovation programs with wildly unrealistic demands for the time it will take to launch something and see revenue – because they want the glory for themselves, not their successors.

Additionally, the business press sensationalizes overnight successes while conveniently ignoring the years of struggle it actually took those entrepreneurs. So corporate leaders – many of whom have never experienced the realities of starting a business from scratch – have completely unrealistic, inflated expectations (two guys in a garage launched Apple…why can’t you???)

Fast, Buzzy Prototypes

In today’s world of digital design and prototyping, it is incredibly fast to make 1 of something (and even a slick marketing campaign to go with it!), but actually launching the product into production, with all the attendant supply chain, quality, service, sales and support demands is brutal. At the beginning of a buzzy new project, it is too soul-crushing for leaders to address that long slog of thankless tasks. This is only made worse by popular business gurus promising all sorts of wacky shortcuts: You’re really in a bad place as a management team if you seriously think you can reach meaningful revenue with an MVP.

Intractable Bureaucracy

Senior leaders often hope that their special little venture team can magically skip all the bureaucracy – most usually by proclaiming from on-high that the innovation team has a mandate to move fast.

But big companies have lots of managers who are charged with legal liability, maintaining brand standards, customer relationships, accounting requirements, ERP systems, reducing SKU counts, so forth — and they don’t want some fast-moving venture team screwing it all up. So of course the rest of the management team isn’t willing to let the precocious innovation program enjoy special privileges and skip the attendant liabilities. It is in these bureaucratic managers’ short-term interest to do nothing – to placate the naïve innovation leaders by telling them that they are eager to support the innovation project — but then not waste any actual effort because everyone knows the project will disappear as soon as the sponsoring executive moves to a new position.

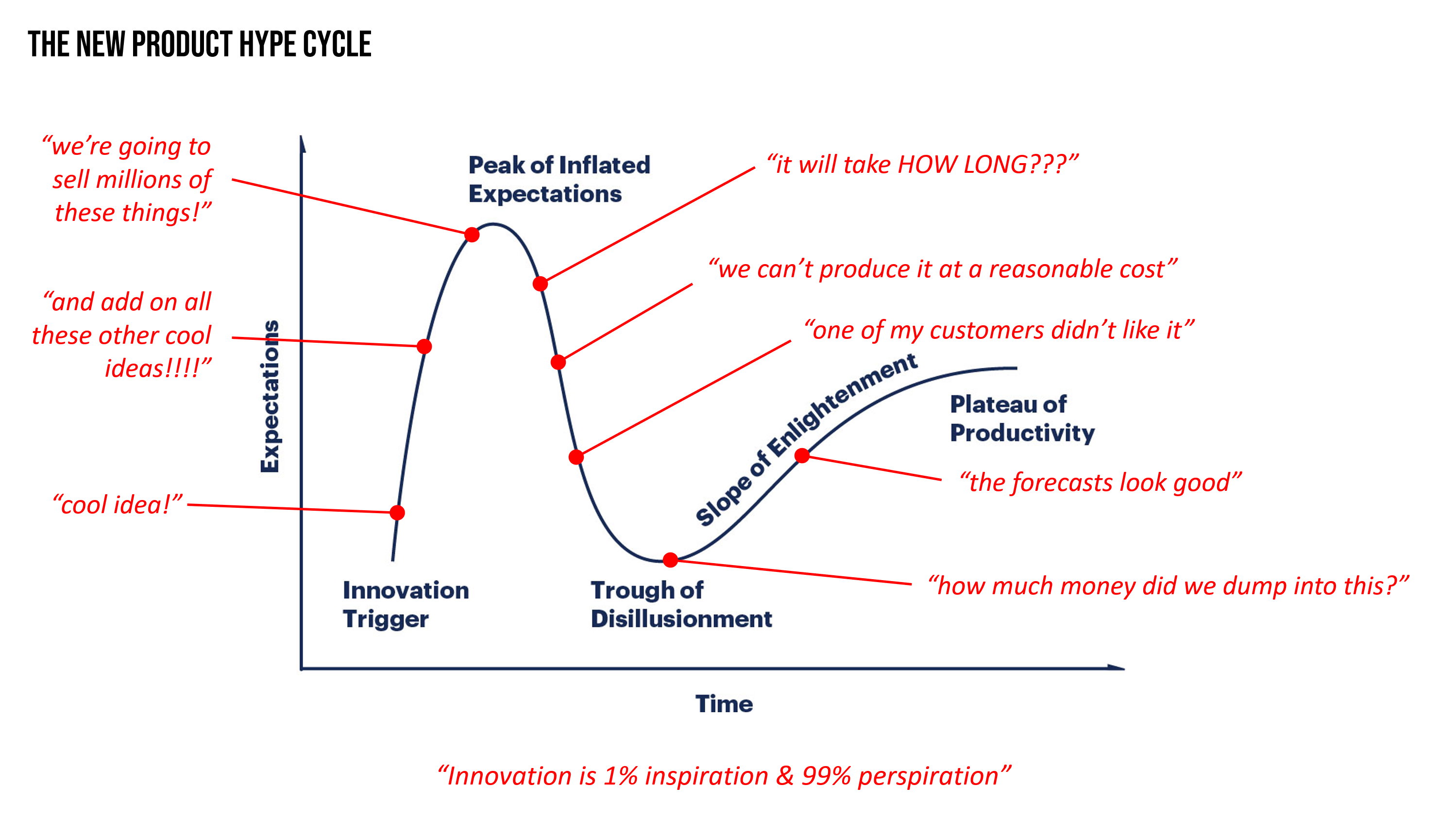

Hype Cycle

New innovation programs are typically ignited by a hype cycle of interest. This is not really a sin of innovation theater, but rather a basic catalyst in launching new endeavors that needs to be recognized and mitigated over time for innovations to succeed. The (in)famous Gartner Hype Cycle, a diagram intended for macro market trends, fits the micro scale of new innovation programs quite well:

You wonder why most innovation programs fail to transfer? The 3 Sins of Innovation Theater allow the devil to surf the hype cycle straight into the Trough of Disillusionment.

Conclusion: The Devil is in the Details

In summary, many new innovation programs are:

1. Catalyzed by unrealistic buzzy expectations. Management teams start projects with grossly inflated expectations of rainbows and unicorns.

2. Grossly under-funded, under-resourced and given ridiculous schedule expectations. Nothing but hot air to puff up the career paths of ascendant managers.

3. Held accountable to ridiculous metrics and precisely compared to imprecise notions of how efficiently the traditional business units perform.

Then just as fast as excitement for a new venture began, the hype cycle collapses when management support for the program encounters even the faintest pangs of reality.

These are the constant challenges that innovation leaders have to recognize and continually work against. Although they are common, the good news is that they are not insurmountable. For ideas on how to structure a solid innovation process, also check out my post What’s the Value of Innovation Management?

The images of corporate innovation purgatory in this article were created by Brad Koerner using Midjourney AI image generation.

About the Author

Brad Koerner is an innovation strategy and R&D program leader with a range of product development, design, marketing and corporate venture experience. Brad has launched new-to-the-world product categories that have earned in excess of $350m. Brad conceived, built and led a corporate venture at a Fortune 500 company, holds 20+ years’ experience spanning global matrix organizations, design consultancies & tech startups, and is an accomplished B2B speaker and writer exploring the future of experiential technologies.